Understanding CPF for PRs in Singapore

Becoming a Permanent Resident in Singapore is a major milestone. But for many of us, CPF only starts to make sense when we begin working — when we realise how it affects our take-home pay, and more importantly, how it supports our future.

A Useful Benefit of Becoming a PR in Singapore

CPF is one of the most important systems to understand as a Permanent Resident, especially once you begin working and planning for your future.

Congratulations on achieving Permanent Residency (PR) in Singapore — a meaningful milestone that opens the door to greater stability and long-term opportunities in this vibrant city.

As a new PR, one of the key benefits you’ll gain access to is the Central Provident Fund (CPF). More than just a savings scheme, CPF plays an important role in supporting your housing, healthcare, and retirement needs. Understanding how it works will help you make informed decisions and fully maximise the advantages that come with your new status.

Why My Salary Felt Lower

The moment CPF becomes noticeable is often the moment working life starts to feel more real.

Initial Confusion

At the beginning, it felt confusing. I knew CPF existed, but I never really understood what it meant in practical terms.

All I noticed was that my take-home pay was lower than expected — like a portion of my salary had disappeared.

Understanding CPF

Over time, I realised that the money wasn’t lost — it was being set aside into CPF.

That shift in understanding changed how I viewed my income. It became less about what I take home today, and more about how I build my future over time.

Snapshot in a Minute

- As a Permanent Resident (PR) in Singapore, you gain access to the Central Provident Fund (CPF) — a comprehensive social security system designed to support your retirement, healthcare, and housing needs.

- Your CPF savings also earn attractive interest rates of up to 6% per annum, helping your funds grow steadily over time.

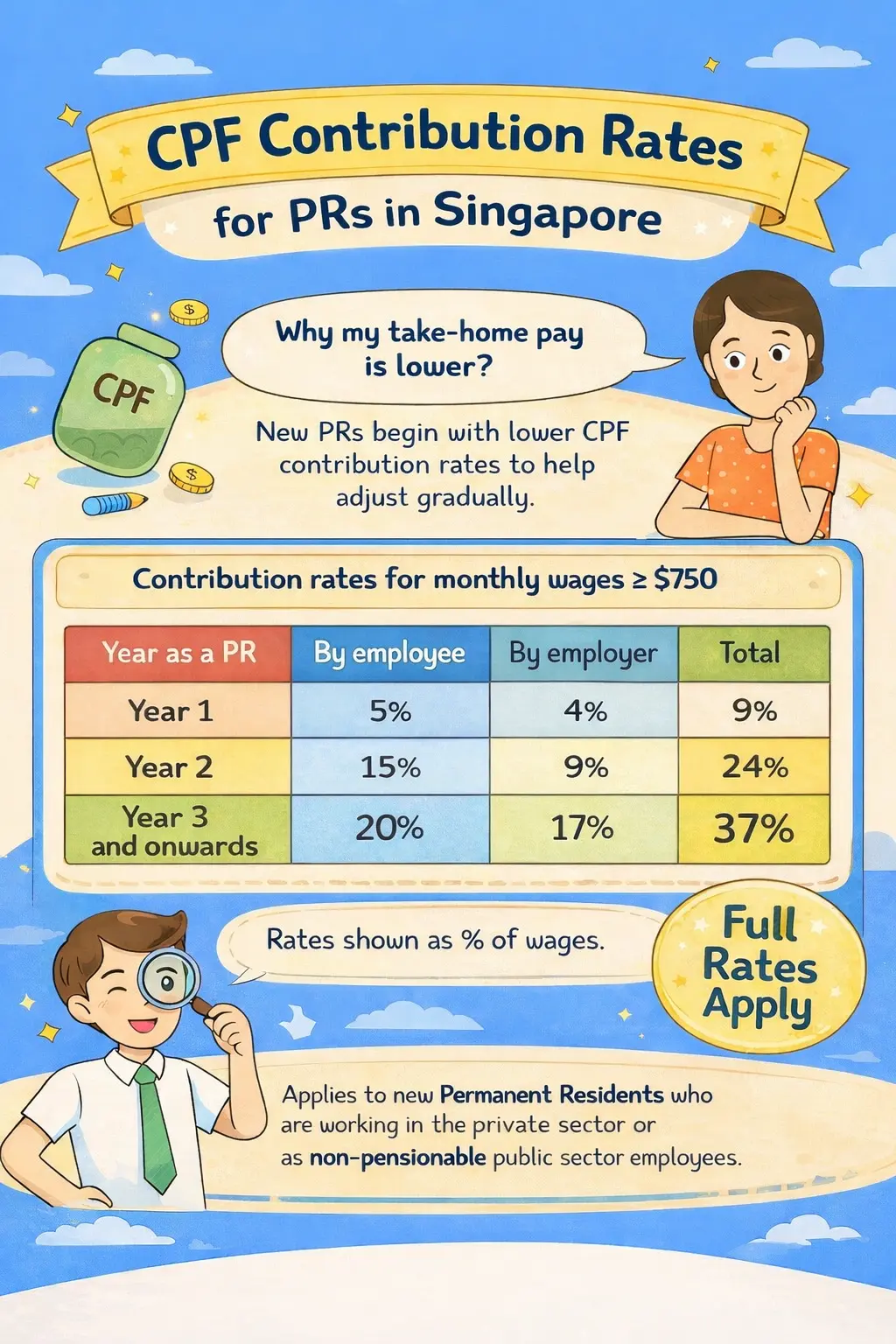

- For new PRs, CPF contributions are implemented on a graduated scale during the first two years. This allows you to ease into the system and adjust gradually to the changes in your take-home pay.

Making Sense of CPF

CPF is not just about setting money aside for retirement — it is a system that helps your savings grow steadily over time to support your retirement, healthcare, and housing needs.

The Central Provident Fund (CPF) is a comprehensive social security system that supports Singapore Citizens and Permanent Residents in meeting their retirement, healthcare, and housing needs. As a PR, participating in CPF can play an important role in strengthening your long-term financial planning.

Your CPF account will be automatically created once you receive your first CPF contribution or make your first top-up. Do remember to inform your employer once your PR status is approved, as CPF contributions become payable from the date you obtain PR status.

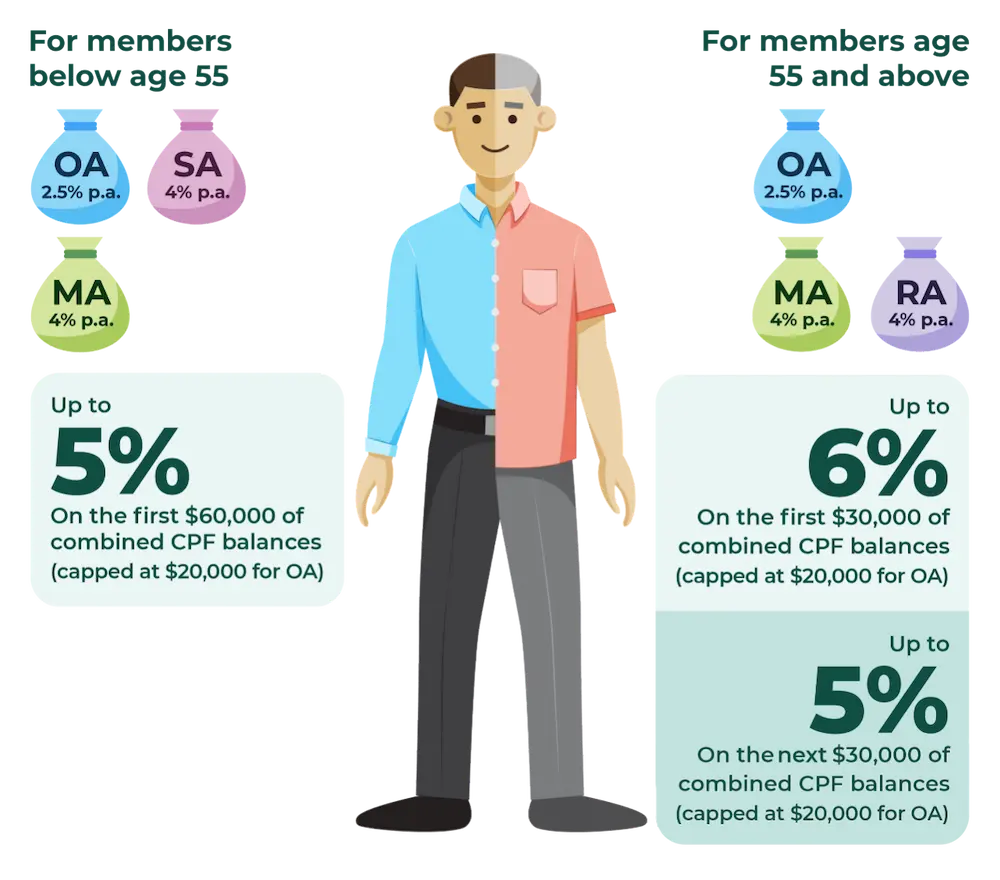

If you are below the age of 55, your monthly contributions are allocated across three main accounts: the Ordinary Account (OA), Special Account (SA), and MediSave Account (MA). Each account serves a distinct purpose, working together to provide you with a well-rounded financial safety net.

The 3 Main CPF Accounts for Members Below 55

Each account plays a different role in supporting your future.

Ordinary Account (OA)

The Ordinary Account is designed for a range of purposes, including retirement savings, housing, investments and specified insurance such as the Dependant Protection Scheme and Housing Protection Scheme.

- Can be used to buy a HDB flat

- Can be used to buy or build private residential properties in Singapore

- Can be used for downpayment, housing loan, stamp duty and legal fees

The CPF Investment Scheme (CPFIS) allows you to invest your OA savings in CPF-approved investments after setting aside S$20,000 in your OA.

Special Account (SA)

The Special Account is dedicated to your retirement savings and investments in retirement-related financial products.

You can invest your SA savings in specified approved products after setting aside S$40,000 in your SA.

The funds in this account are meant to support you in your later years, ensuring that you have sufficient nest egg to maintain your standard of living during retirement.

MediSave Account (MA)

The MediSave Account is used to cover medical expenses and approved medical insurance premiums.

As healthcare costs can be significant, especially as you age, having a dedicated account for medical expenses provides peace of mind.

How CPF Savings Grow Over Time

One of the standout features of CPF is its attractive interest rates, which help your savings grow over time.

OA Base Rate

SA / MA / RA Base Rate

For Members Below Age 55

- First S$60,000 earns an extra +1% interest (up to S$20,000 from OA)

- Effective rates of up to 5%

💡 Risk-free and compounded — your savings grow steadily without market risk.

For Members Aged 55 and Above

- Up to 6% p.a. on first S$30,000

- Up to 5% p.a. on next S$30,000

- Includes up to S$20,000 from OA

WHY YOUR TAKE-HOME PAY CHANGES AS A NEW PR

Contributions are introduced gradually to help you adjust to changes in take-home pay.

CPF Contribution Rates for New PRs aged 55 and below

New Permanent Residents do not start at full CPF contribution rates immediately. The rates are introduced gradually during the first two years to help ease the adjustment in take-home pay.

For PRs aged 55 and below, the total contribution rate rises from 9% in Year 1, to 24% in Year 2, and reaches the full 37% from Year 3 onwards.

You and your employer may also jointly apply to the CPF Board to contribute at higher rates earlier if you prefer to build your CPF savings more quickly.

For members above age 55, contribution rates also follow a graduated scale, but differ depending on your age band. Refer to CPF’s official website for the latest breakdown.

💡 Full CPF contribution rates apply from Year 3 onwards.

How CPF LIFE Supports Your Retirement

Lifelong monthly payouts to help reduce the risk of outliving your savings.

CPF LIFE is a national longevity insurance scheme that provides lifelong monthly payouts, which you can start anytime from age 65.

Monthly payout amounts depend on how much retirement savings you have set aside and the CPF LIFE plan you choose.

There are 3 CPF LIFE plans: Escalating, Standard and Basic.

Escalating Plan

Monthly payouts start lower but increase over time, helping you keep up with rising living costs.

Standard Plan

Provides stable monthly payouts throughout retirement.

Basic Plan

Monthly payouts start lower and may decrease over time.

FRS at age 55 for 2026

ERS at age 55 for 2026

Retirement Sum at Age 55

| Year | BRS | FRS | ERS |

|---|---|---|---|

| 2024 | S$102,900 | S$205,800 | S$308,700 |

| 2025 | S$106,500 | S$213,000 | S$426,000 |

| 2026 | S$110,200 | S$220,400 | S$440,800 |

| 2027 | S$114,100 | S$228,200 | S$456,400 |

Retirement sums increase over time to account for rising living costs.

FRS - Standard Plan Example

If you set aside the Full Retirement Sum (FRS) of S$220,400 at age 55 in 2026, you can expect lifelong monthly payouts of about S$1,780 from age 65 under the Standard Plan.

ERS - Standard Plan Example

If you set aside the Enhanced Retirement Sum (ERS) of S$440,800 at age 55 in 2026, you can expect CPF LIFE monthly payouts of about S$3,440 from age 65 under the Standard Plan.

Want to see how CPF LIFE payouts are estimated?

Refer to CPF’s official payout breakdown →Basic Insurance Coverage

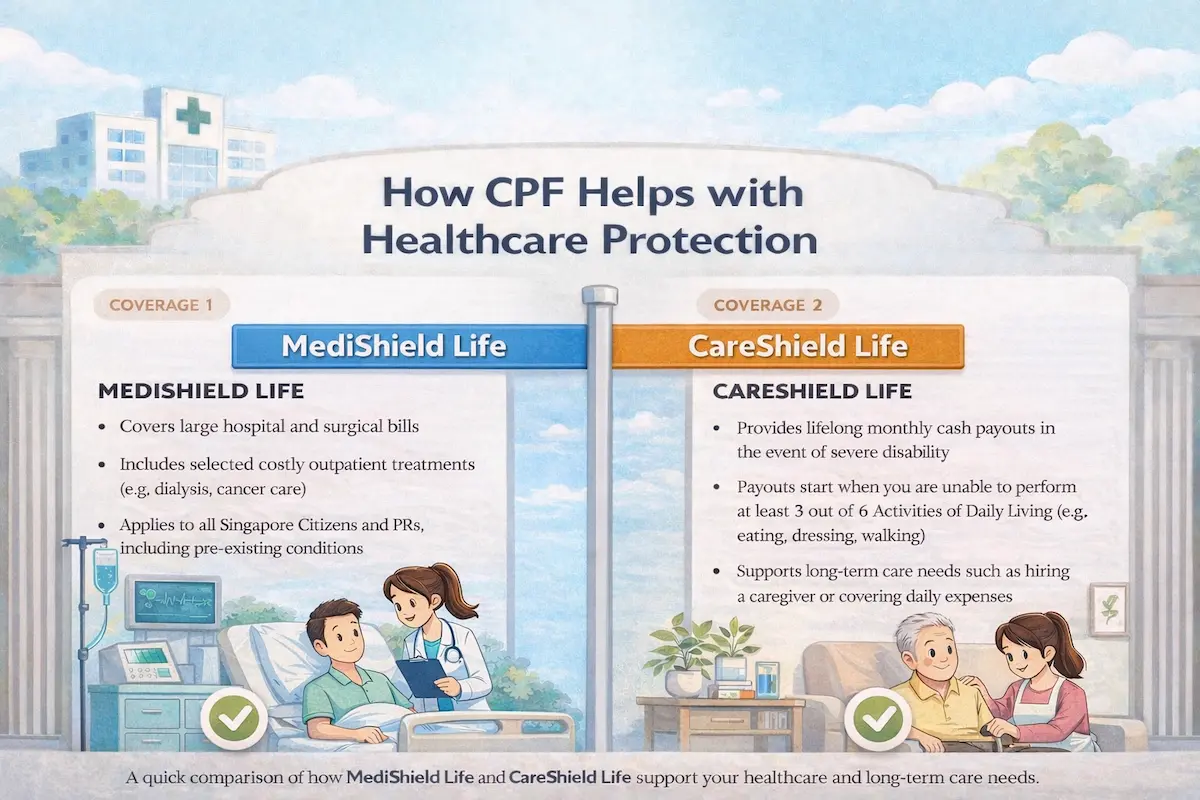

CPF also supports hospitalisation and long-term care needs through national insurance schemes.

MediShield Life

- Covers large hospital and surgical bills

- Includes selected costly outpatient treatments (e.g. dialysis, cancer care)

- Applies to all Singapore Citizens and PRs, including pre-existing conditions

Coverage is sized for subsidised wards in public hospitals (B2/C). Higher ward classes or private hospitals are still covered, but with lower payouts.

Premiums can be fully paid using your MediSave account.

CareShield Life

- Provides lifelong monthly cash payouts in the event of severe disability

- Payouts start when you are unable to perform at least 3 out of 6 Activities of Daily Living

- Supports long-term care needs such as hiring a caregiver or covering daily expenses

CareShield Life provides lifelong monthly cash payouts in the event of severe disability. It is mandatory for Singapore Citizens and Permanent Residents born in 1980 or later, while some older cohorts may be covered under transition arrangements.

In Conclusion

Understanding CPF helps you make better decisions about your future in Singapore.

Retirement

CPF helps you build long-term savings and provides lifelong monthly payouts through CPF LIFE.

Healthcare

MediSave, MediShield Life and CareShield Life help support medical and care-related needs over time.

Housing

The Ordinary Account can support downpayment, housing loans and related costs, making CPF especially relevant when planning for a home.

Not Sure How CPF Fits Into Your Journey?

If you are unsure how CPF connects to your housing plans or when to start thinking about your first home, let’s go through it step by step.

- © 2026 Shermynn Lee R071920B

- All rights reserved